In its continuing bid to cool down raging inflation in the United States — at 9.1% in June, the inflation rate is at a four-decade high — the Federal Reserve or Fed (US’ central bank) decided to raise the Federal Funds Rate target by another 75 basis points on Wednesday. Since March, the Fed has steadily pushed up the targeted FFR from zero to almost 2.5% now.

What is the Federal Funds Rate (FFR)?

The FFR is the interest rate at which commercial banks in the US borrow from each other overnight. The US Fed can’t directly specify the FFR but it tries to “target” the rate by controlling the money supply. As such, when the Fed wants to raise the prevailing interest rates in the US economy, it reduces the money supply, thus forcing every lender in the economy to charge higher interest rates. The process starts with commercial banks charging higher to lend to each other for overnight loans.

Why is the Fed tightening money supply?

This is called monetary tightening, and the Fed (or any other central bank, for that matter) resorts to it when it wants to rein in inflation in the economy. By decreasing the amount of money, as well as raising its price (the interest rate), the Fed hopes to dent the overall demand in the economy. Reduced demand for goods and services is expected to bring down inflation.

What are the risks of monetary tightening?

Aggressive monetary tightening — like the one currently underway in the US — involves large increases in the interest rates in a relatively short period of time, and it runs the risk of creating a recession. This is called a hard-landing of the economy as against a soft landing (which essentially refers to monetary tightening not leading to a recession). The chances of a soft-landing for the US exist but are extremely low.

Subscriber Only Stories

The most common definition of recession requires the GDP of a country to contract in two successive quarters. Contracting GDP typically results in job losses, reduced incomes, and reduced consumption.

So, is the US in recession?

A firm answer may be available as early as 6 pm India time, when the US announces the GDP growth data for the second quarter (April, May and June) of 2022. Since the US GDP has already contracted by 1.6% during the first quarter (January, February and March) of 2022, a contraction in the second quarter will imply the US is in recession (see Chart 1).

Chart 1: US real GDP

However, many observers also contest this rather strict technical definition of recession.

Why are some people contesting that the US might be in recession?

For one, there is a chance that the US GDP may not contract. If that happens, the whole point is moot for the time being. We will know this at 6 pm (IST) on Thursday.

But there are other reasons.

A massive point of contradiction is the remarkable job creation in the first half of 2022. Notwithstanding the Fed’s aggressive monetary tightening, the labour market remains quite “tight” — that is, unemployment still remains at historic lows. In fact, despite a contraction in GDP in the first quarter and a likely contraction in the second quarter, the US economy created around 2.7 million new jobs in the first half of 2022. This is more than the number of jobs created in any full-year period in the recent past.

This is the reason why Fed Chairman Jay Powell refused to characterise the US economy as one undergoing recession when asked during the media interaction on Wednesday. Janet Yellen, US Secretary of the Treasury (as well as a former chair of the Fed), has also argued that the US economy is not in recession even if the GDP contracts for two successive quarters.

This leads to a broader issue of how one defines a recession.

In the US, it is the National Bureau of Economic Research (NBER) — more specifically, the NBER’s Business Cycle Dating Committee — that typically declares a recession. But the NBER defines recession a little differently.

How does NBER define recession?

The NBER’s traditional definition of a recession is that “it is a significant decline in economic activity that is spread across the economy and that lasts more than a few months”. The committee’s view is that while each of the three criteria—depth, diffusion, and duration—needs to be met individually to some degree, extreme conditions revealed by one criterion may partially offset weaker indications from another.

Why doesn’t the NBER accept the two quarters definition?

The NBER gives several reasons for it.

“First, we do not identify economic activity solely with real GDP, but consider a range of indicators. Second, we consider the depth of the decline in economic activity… Thus real GDP could decline by relatively small amounts in two consecutive quarters without warranting the determination that a peak had occurred. Third, our main focus is on the monthly chronology, which requires consideration of monthly indicators. Fourth, in examining the behavior of production on a quarterly basis, where real GDP data are available, we give equal weight to real GDI,” states the NBER website. The GDI refers to gross domestic income; this is also a measure of national income albeit from the income side of the economy as against the GDP, which looks at the expenditure side of the economy.

According to NBER, the difference between GDP and GDI—called the ‘statistical discrepancy’—was particularly important in the recessions of 2001 and 2007–2009.

How did GDP and GDI differ in the recessions of 2001 and 2007-09?

In 2001, for example, the recession did not include two consecutive quarters of decline in real GDP. However, Real GDI declined for the final three quarters of 2001.

In the latter case of recession, from the peak in December 2007 to the trough in June 2009, real GDP declined in the first, third, and fourth quarters of 2008, and in the first and second quarters of 2009, while GDI declined for five of the six quarters.

What is the outlook for the US economy?

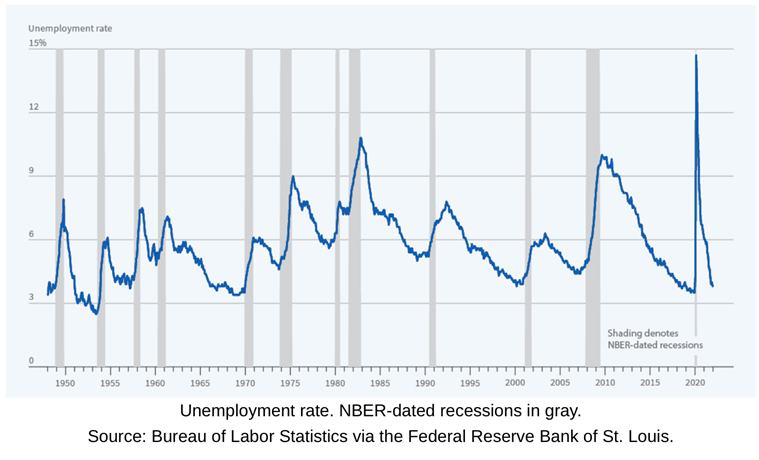

The US economy is facing a curious situation. One the one hand, it faces an inflation rate that is at a four-decade high and, on the other, its unemployment rate is at five-decade low (see Chart 2).

However, aggressive monetary tightening of the kind being witnessed will likely result in a recession sooner rather than later.

The US inflation rate is at over 9% and the Fed’s target inflation rate is 2% — that’s a gap of 7 percentage points. Historically, every time the Fed has tried to bring down inflation by more than 2 percentage points, the US has witnessed a recession.

The ongoing inversion of the bond yield curve is another robust predictor of a recession in the offing. As of Wednesday, the yields on 2-year, 5-year and 10-year US bonds were 2.97%, 2.83% and 2.78%, respectively.

In his statement on Wednesday, Powell made no bones about the Fed’s determination to bring inflation under control even at the cost of destroying economic growth and raising unemployment in the short term.

“We are highly attentive to inflation risks and determined to take the measures necessary to return inflation to our 2 percent longer-run goal. This process is likely to involve a period of below- trend economic growth and some softening in labor market conditions, but such outcomes are likely necessary to restore price stability and to set the stage for achieving maximum employment and stable prices over the longer-run,” he stated.

In other words, the Fed believes that the risks of doing too little (to contain inflation) are higher than the risks of doing too much (i.e. destroying demand).

What is the likely impact on India?

In the latest — July update of the — World Economic Outlook, the IMF has downgraded the growth projections for the US, China and India. “Downgrades for China and the United States, as well as for India, are driving the downward revisions to global growth during 2022–23, which reflect the materialization of downside risks highlighted in the April 2022 World Economic Outlook,” it states.

A global slowdown is unlikely to have any positives for India apart from some relief in crude oil prices.

The IMF has knocked off almost a full percentage point each (0.8%, to be precise) off India’s GDP projections for the current year and the next.

“For India, the revision reflects mainly less favorable external conditions and more rapid policy tightening,” explains the IMF.