Jitendra Gupta | Nitin Agrawal | Bharat Gianani | Anubhav Sahu

Highlights

– Carving out of O2C subsidiary provides scope for improved capital allocation and asset monetization

– Oil & Gas: Towards new energy mix

– Telecom: Strong cash flow prospects in what is almost a duopoly

– Retail: Recent acquisitions & online forays present significant synergies

– Net debt substantially reduced in FY21; Fund raised preps RIL to invest behind new age businesses- Presents case for re-rating

————————-

Reliance Industries (RIL) (CMP: Rs 2,021; Mcap: Rs 13,09,869 crore) has announced carving out its O2C (oil to chemicals) business as a separate 100 per cent subsidiary, subject to regulatory approvals. This brings a sharper focus to the fourth leg of growth – O2C, the downstream business – in terms of capital allocation and asset monetization. The other legs are Oil & Gas, Telecom and Retail.

This also redefines RIL’s goal for O2C and Oil & Gas businesses towards new age energy and materials and potentially presents a case for re-rating of these businesses. The differentiated structure also augurs well for consumer facing businesses – Jio & Retail – in terms of value unlocking, as and when there is a separate listing.

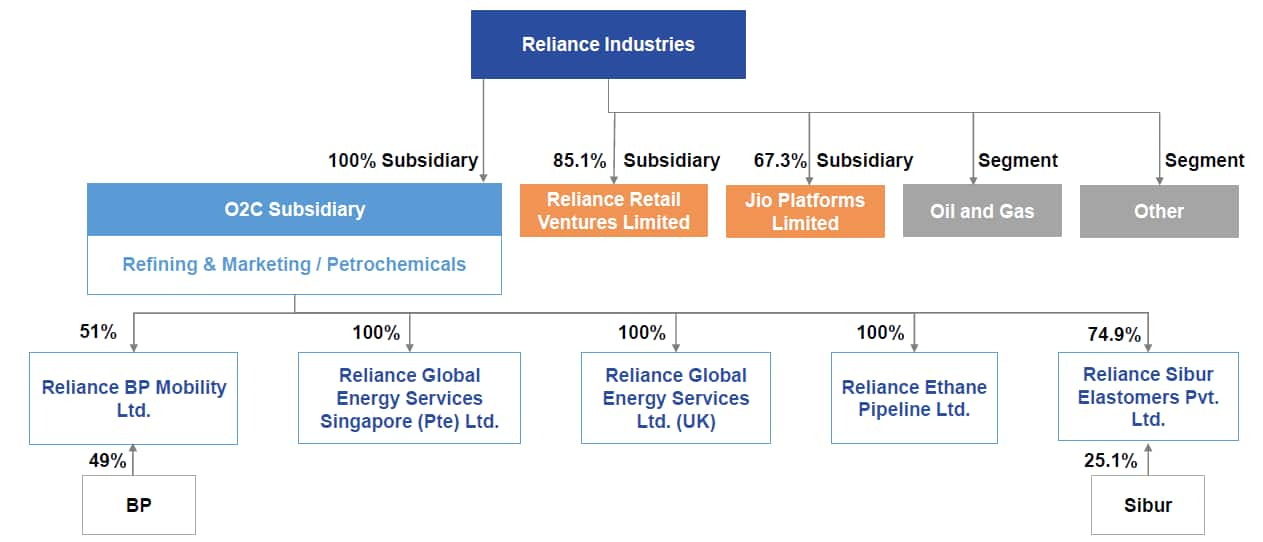

What does it mean for O2C?

Proposed structure

Source: RIL

Currently, O2C business accounts for close to 30 percent of the group’s consolidated assets but contributes 67 percent to the company’s consolidated operating revenue. Since there are no changes in the shareholding pattern post this exercise, the economic benefit will still remain with RIL shareholders. Benefits would largely come in terms of focused capital allocation, investment behind new age materials and asset monetization.

Greater focus on capital allocation

Part of the assets which will be transferred to the subsidiary will be funded through a $25 billion loan (total group borrowings $35 billion) from RIL on a floating rate of interest linked to the SBI MCLR rate.

This essentially means part of the group debt will be transferred to the O2C business, which will be supported by its own cash flows, assets and future profits.

This will bring in a sharper focus when making capital allocation decisions. In future, the subsidiary structure, as a focused business, could allow it to use its own growth capital independently to pursue growth opportunities and create value.

Becoming future ready

The O2C business has a presence across the value chain, from oil to chemicals. The company intends to maximize or leverage the conversion cycle from oil to chemicals to materials in the entire value chain. It has several growth and futuristic plans such as developing a green energy ecosystem, renewables, carbon capture and storage technologies and transition from the traditional carbon-based fuels to a hydrogen economy.

The subsidiary structure can allow O2C business to leverage its own capital to pursue growth projects. Moreover, investors would impute more value to a simpler and focused entity that allows the subsidiary to independently use its own cash flows, raise growth capital and bring strategic investors. In future, the new structure would provide subsidiaries much more leeway in terms of forming alliances, JVs and bring growth partners as well as get a separate listing (if needed) on the exchanges, providing investors a clear choice of business to invest in.

Oil & Gas: Towards new energy mix

Gas with its low carbon footprint will continue to play a key role as a transition fuel. RIL and BP have recently announced the start of production from the R Cluster, ultra-deep-water gas field in block KG D6 off the east coast of India. RIL and BP are developing three deep water gas projects in block KG D6, which together are expected to meet ~15 percent of India’s gas demand by 2023.

Retail: Significant synergy benefits under way

In its retail foray, RIL has been ahead of the curve with a faster store expansion strategy. What is important is the integration of the online and the offline strategy particularly in the grocery and the apparel segment, which will be instrumental in Reliance Retail growing at a faster clip and provide a distinct competitive advantage.

Venturing into new areas such as online pharmacy and home decor solutions would be a key growth driver. The company has acquired a controlling stake in Netmeds as well as Urban Ladder Home Décor Solutions.

The proposed acquisition of the Future group assets would strengthen its exposure in segments such as grocery, fashion and lifestyle. Also, the earnings per unit of the Future group assets is below par and Reliance with its huge scale and strong online capabilities can improve profitability, leading to further value accretion. With the transaction at a much lower EV/EBIDTA multiple of 6.7x, it is a value accretive acquisition. With the successful integration of Jio Mart and AJio fashion with Future’s assets, profitability is expected to improve further.

Telecom: Benefiting from what is practically a duopoly

In a short span of less than four years, Jio has become the largest digital service provider in India with a 410 million subscriber base. It is also the first operator to cross 400 million subscribers in a single country market. The strong footing of RIL’s digital business is also evident from the significant financial and strategic investment made by marquee investors including Facebook and Google.

The outlook for Jio Platforms continues to be very strong with rising ARPU (average revenue per user) and increase in data consumption, due to trends such as work from home and people watching more content online. The launch of JioGigaFiber services has also seen increased uptake. Other digital platform services such as JioMeet, Jio’s bundled broadband offering for small and medium businesses, IoT (Internet of Things) solutions for Jio Home users are also getting encouraging response from its customers.

Outlook

Till recently, the focus was on two aspects: deleveraging & value unlocking for two growth engines – the retail & telecom businesses. In the last one year, a series of fund raising programs – rights issue and bulge-bracket deals in quick succession for both Jio and Reliance Retail–have been largely in pursuit of this focus. The amount raised so far for Reliance Retail has been Rs 47,265 crore for ~10 percent stake in the Reliance retail venture, while that for Jio Platform has been Rs 1,52,056 crore after an equity dilution of 33 percent.

Now, the proposed reorganisation of the O2C business adds to the prospect of raising growth capital, which in turn would serve as a catalyst for the legacy growth engine. This would accelerate asset monetization efforts (pending Aramco deal and others) and investment towards new age energy and materials. The creation of a pure-play O2C platform will attract focused strategic partners and capital in times to come.

Note that recently the company has entered into a definitive agreement for making capital contribution, up to USD 50 million, in Breakthrough Energy Ventures II, L.P. The Fund will have special focus on “tougher climate challenges” in greener steel and cement, long-haul transport, direct air capture and hydrogen. Success in these ventures should help transform RIL’s new energy and material businesses. We believe the new structure will help incubate similar growth platforms.

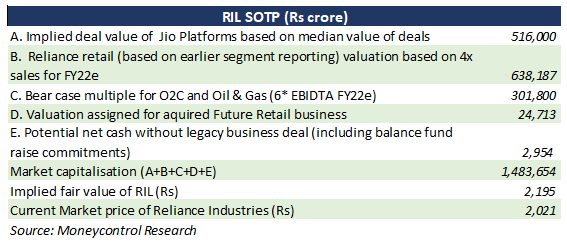

This will also add to RIL’s vision of being net carbon zero by 2035 by pursuing renewable energy goals, transition to a hydrogen economy, energy storage technologies and developing a portfolio of advanced and specialty materials. We believe therefore that the current valuation assigned to the O2C/Oil & Gas businesses has significant scope for an upside re-rating.

Disclaimer: Reliance Industries Ltd., which also owns Jio, is the sole beneficiary of Independent Media Trust which controls Network18 Media & Investments Ltd.