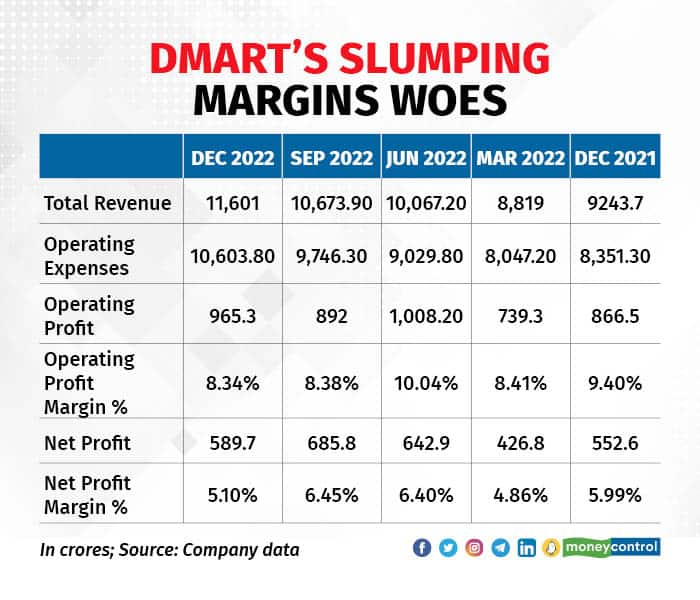

Thinning profit margins at Avenue Supermarts, the owner and operator of D-Mart stores, are worrying investors after the company’s net profit in the December quarter missed analyst estimates.

The retailer’s operating profit margin shrank to 8.34 percent from 8.38 percent in the quarter ended September. While the fall was almost negligible, the operating profit margin was the lowest in six quarters.

Gross profit margin also came under pressure. At 14.8 percent, the gross profit margin was down by 60 bps YoY and 30 bps QoQ.

Shares of Avenue Supermarts have fallen 6% since the earnings were reported on January 14.

Neville Noronha, managing director of Avenue Supermarts, indicated that the decline in the gross margins was due to falling sales in the general merchandise and apparel segments.

“FMCG and staples segment continued to outperform the general merchandise and apparel segments. The gross margin percentage decline over the corresponding quarter of last year is a reflection of this mix change. Discretionary non-FMCG sales did not do as well as expected in this quarter,” Noronha said.

An intractable fall in the discretionary segment would continue to box in the profit margin for the retailer, which will have to find new ways of cutting costs to keep margins buoyant.

Inflation and competition

“Inflationary stress acutely impacting mass discretionary consumption as well as low footfalls impacting impulse purchase were highlighted by management as possible reasons for a weak mix last quarter. These headwinds seemed to have continued in Q3FY22 as well,” investment banking firm Jefferies said in a research report.

However, apart from inflation, D-Mart will have to brave headwinds from intensifying competition and gradually weakening unit economics.

“On the back of festive purchases in the GM & apparel segment, Q3 generally tends to yield gross margins in excess of 15 percent. However multiyear low margins recorded in Q3FY23 reflect some grave challenges, which could possibly be on account of heightened competitive intensity over the past two years and inflationary stress still pertaining in the discretionary value segment,” ICICI Direct Research said in its report.

According to HDFC Securities, “D-Mart’s weaker unit economics (than usual) is not just a function of high inflation keeping discretionary purchases in check but also a consequence of a fair challenge to D-Mart’s value proposition by deep-pocketed peers within D-Mart’s top districts.”

For the near term, one redeeming factor could be that inflationary pressures could be in retreat. Retail inflation for December came in at 5.72 percent compared with 5.88 percent in November.

DMart’s slumping margins woes

SBI Research pointed out that retail inflation could ease to 5 percent levels by March 2023. With the fall in inflationary pressures, D-Mart might be able to bolster discretionary consumption in the coming quarters.

There are other hitches. Per-store revenue for the hypermarket chain registered a rather conservative three-year CAGR growth of 2 percent.

“Per-store revenue growth was muted at 4 percent y-o-y, as discretionary non-FMCG/grocery sales remained soft. 3Y CAGR in per-store revenues were also modest at 2 percent. Per-sq. ft. revenues declined 2 percent YoY with 3Y CAGR at (-3 percent), as D-Mart is incrementally adding larger area stores, while per-store revenues remained muted,” Jefferies said.

Avenue Supermarts added four stores in the third quarter, taking the total to 22 in the first nine months of FY23. It will need to open 28 stores in the last quarter to match last year’s 50 store addition number.

Past perfect, future tense

Should investors stay loyal to the retailer, which has delivered handsome returns over the past two-three years?

HDFC Securities does not share the unbridled optimism of the loyal force of the company’s retail as well as institutional investors. It has a ‘sell’ recommendation for the retailer with a target price of Rs 3,000 given its suboptimal unit economics and heightened competitive intensity.

ICICI Direct Research is looking at a glass-half-full situation and has pushed a ‘hold’ recommendation on the retailer with a target price of Rs 4,000.

It said Avenue Supermarts has been a consistent compounder with the stock price increasing 27 percent CAGR in the past five years. However, since last year, the stock has delivered negative returns of 12 percent as the revenue trajectory tapered down to 19-20 percent vs. 25-30 percent and the product mix change led to lower-than-expected margins.

“D-Mart continues to remain India’s most profitable low-cost retailer, a strong play on India’s retail growth story and a key beneficiary of the unorganised to organised segment shift,” ICICI Direct Research said. “We introduce FY25E estimates and bake in earnings CAGR of 22 percent in FY23-25E (vs. CAGR of 24 percent witnessed in FY20-23E).”