ExplainSpeaking-Economy is a weekly newsletter by Udit Misra, delivered in your inbox every Monday morning. Click here to subscribe

Dear Readers,

In just three weeks’ time — on February 1, to be precise — Finance Minister Nirmala Sitharaman will rise to present the Union Budget for the next financial year (2023-24). This is going to be a crucial Budget as it is likely to be the last full-fledged Budget of the incumbent government.

But before deciding on how much to spend on what scheme and where to raise the money from, the Finance Minsiter needs to know the rate at which the economy is likely to grow in that year (2023-24). But this growth rate can only be an assumption.

Subscriber Only Stories

Even so, what does the Finance Minister base this assumption on?

Well, she would have to look at the GDP growth rate of the current financial year (2022-23) and firm up her plans.

But the current financial year will end in March. So how can the FM know what the growth rate will be?

First Advance Estimates (FAE)

It is here that something called the First Advance Estimates (FAE) of GDP comes into the picture. The MoSPI released the latest FAE (for 2022-23) on January 6.

Advertisement

Since 2016-17, each year, the Ministry of Statistics and Programme Implementation (MoSPI) releases the FAE at the end of the first week of January.

They are the “first” official estimates of how GDP is expected to grow in that financial year. But they are also the “advance” estimates because they are published long before the financial year (April to March) is over. It is also important to note that even though the FAE are published soon after the end of the third quarter (October, November, December), they do not include the formal Q3 GDP data; the Q3 data is published at the end of February as part of the Second Advance Estimates (SAE).

In other words, the FAE serve a specific role: They serve as the GDP estimates that the Union Finance Ministry uses to decide the next financial year’s budget allocations. Of course, the FAE are overtaken by the SAE by the end of February.

Advertisement

FAE’s significance; nominal GDP vs real GDP

There are two ways to look at the FAE.

One is to look for the “nominal” GDP growth rate; this is the rate of growth that is observed and includes the effect of prices. The nominal growth rate is the one used to decide the next year’s Budget allocation.

The second way to look at the FAE is to look for the “real” GDP growth data; that is, the growth once we remove the effects of inflation. Looking at the real GDP data tells you what has been happening in the economy in “real” terms.

Suppose India produced only one thing — say bananas — and all its GDP came from the production of bananas. Imagine that the price of bananas doubled between the last financial year and the current financial year; in other words, the inflation rate was 100%. Further, imagine that the total number of actual bananas produced remained the same across both years.

In such a scenario, the nominal GDP will show a growth rate of 100% while the real GDP growth rate will be zero per cent.

Advertisement

Here’s another way to remember the link between the two:

Real GDP growth rate = Nominal GDP growth rate — Inflation Rate

How are the FAE arrived at?

Advertisement

Since the year is still far from being over, the FAE are based on a lot of extrapolation — that’s when you take data for the first 6 or 7 months and project a full-year number based on some calculations.

MoSPI states the FAE are “compiled using the Benchmark-Indicator Method i.e. the estimates available for the previous year (2021-22 in this case) are extrapolated using relevant indicators reflecting the performance of sectors.”

Advertisement

For instance, it uses the sale of commercial vehicles data up to September and the same of passenger vehicles data up to November.

So what did the latest FAE show?

Nominal GDP

India’s nominal GDP is set to grow by 15% in the current financial year. While this is an impressive number, it is lower than the 20% growth in 2021-22. Moreover, it is also noteworthy that a large part of this nominal growth is a result of the high prices (read inflation). In fact, inflation contributed to a majority of the nominal GDP growth since the real GDP growth rate is expected to be just 7%.

In times of high inflation, borrowers of money tend to benefit because inflation essentially means that money is losing value. As such, if you borrowed Rs 100 in one year and then inflation went up, it implies that the Rs 100 you return are of lower “value” than the Rs 100 you borrowed initially. That’s because the hundred you borrowed had a higher purchasing power than the hundred you return, thanks to inflation.

Government, which is the biggest single borrower in the economy, benefits from inflation. Since all debt metrics are in terms of nominal GDP, if nominal GDP goes up primarily due to high inflation, governments tend to find that their debt-to-GDP metrics improve.

While all this is great news for the current year, looking ahead, experts expect India’s nominal GDP growth rate to decelerate sharply yet again in 2023-24. Nomura expects nominal GDP growth to slow down to just over 10% while Motilal Oswal expects it to grow by just 7.5% in the coming year. That, in turn, implies worsening debt metrics for the government. Slower nominal growth also suggests an even lower growth rate for India’s real GDP.

Real GDP and real GVA

The FAE suggest that in the current financial year, real GVA (gross value added) and real GDP (gross domestic product) — the two main ways to measure India’s national income — will grow by 6.7% and 7%, respectively.

By themselves, these numbers may seem impressive; even more so when compared internationally. But international comparisons are of limited value.

What truly matters is the home truth, or the level of domestic growth because the developed countries such as the US and UK or even China for that matter are much richer in per capita terms and India needs to grow at a much faster rate. Moreover, annual growth rates have lost their usual significance because the base became remarkably low after the contraction in the economy during Covid.

The way to understand how India’s growth has been on aggregate is to compare the absolute levels of GVA and GDP at the end of FY23 (that ends in March) and see how much growth we have registered over the FY20 (pre-Covid) level. That growth number will give a sense of where we are placed.

TABLE 1 provides the absolute levels of GVA and GDP. The last row tabulates the growth rate over the past three years. It shows that both real GVA and GDP have grown by just about 10% over the past three years (that is, compared to the pre-Covid year).

Table 1: Absolute levels of GVA and GDP, from FY 2015 to FY 2023.

To see this growth in perspective, remember that past finance ministers have talked about the need for India to grow at 9%-10% every year while this is the growth over 3 years. It just captures the loss of at least two full years of economic growth and while this may not affect the people who earn over Rs 10 or 12 lakh per annum, this loss of growth has a huge adverse impact on the consumption levels and well-being of those Indians who are relatively poorer.

Engines of Growth

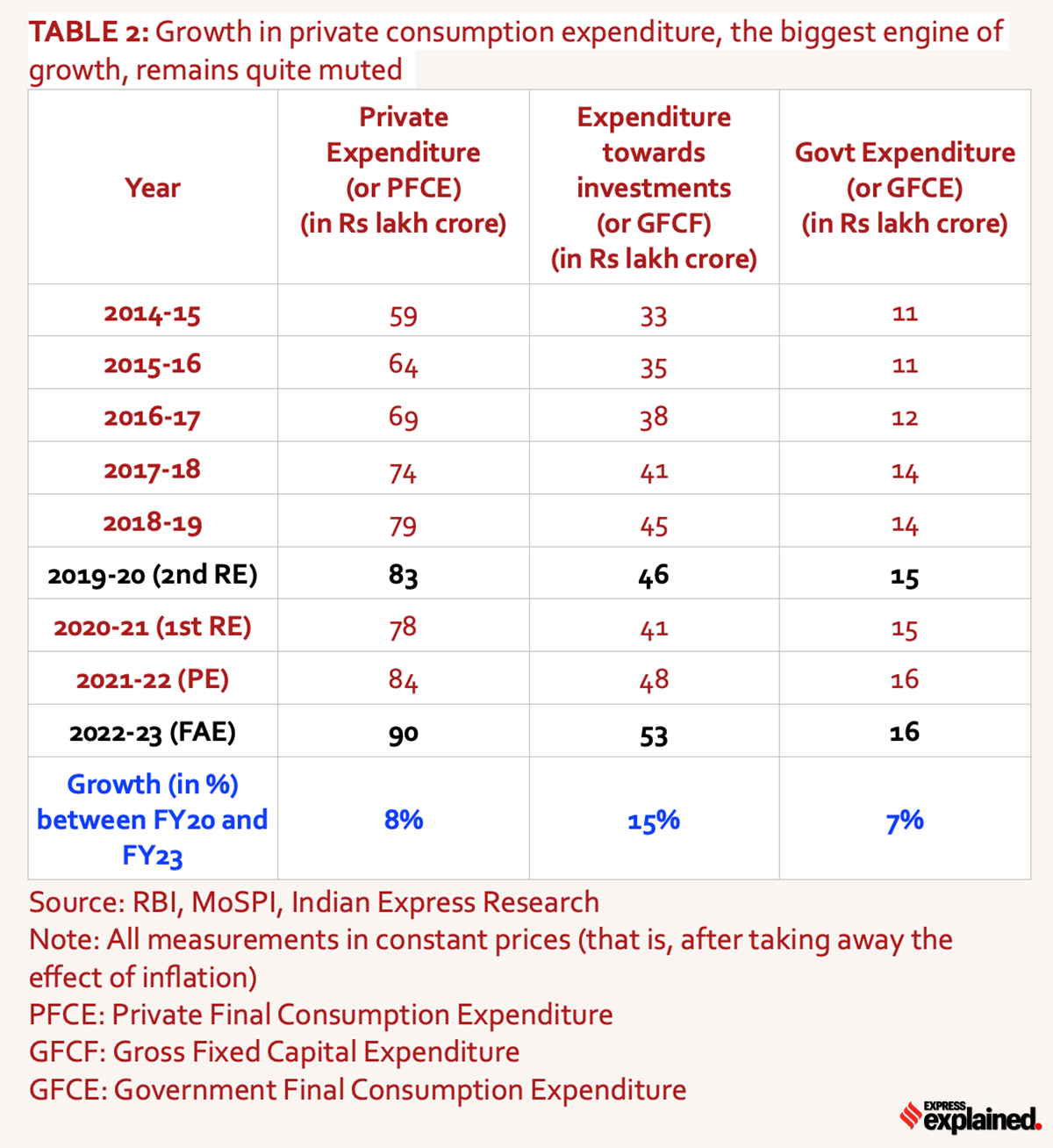

India’s GDP has three main drivers.

Expenditures made by people in their private capacity towards their consumption is the biggest engine, accounting for 56% of all GDP.

Expenditures made towards investments (both by private firms and the government) are the second biggest engine, accounting for 33% of all GDP.

The government’s expenditure towards everyday items such as salaries accounts for the remaining 11%.

As TABLE 2 shows, private consumption expenditures have barely grown. The growth is just 8% over the past three financial years. Government expenditure is even more stagnant. Investment expenditures have grown slightly better, but as Pranjul Bhandari of HSBC pointed out in the year-end special episode of The Express Economist, most of this expenditure is just to replace the old investment, not the fresh one.

Table 2: Private consumption expenditure, fixed capital expenditure and government consumption expenditure from FY 15 to FY 23.

Table 2: Private consumption expenditure, fixed capital expenditure and government consumption expenditure from FY 15 to FY 23.

Sectoral health of the economy

Disaggregated GVA data compiled in TABLE 3 provides a sense of how the different sectors of the economy might be placed at the end of FY23. It is important to note not just the size of contribution a sector makes in money terms but also how many jobs a sector creates.

Table 3: Growth over the last three years for various sectors

Table 3: Growth over the last three years for various sectors

For instance, services such as trade, hotel, transport etc. are expected to be barely 1% above the pre-Covid level. Think of all the small operators in these sectors and the job and income losses that may have occurred. The recovery figures are aggregate; the informal sector is likely to be in much greater pain than what this 1% growth over three years suggests.

Similarly, ‘mining and quarrying’ is another sector that creates several, albeit low-quality, jobs. It, too, is still struggling.

That is not to say that sectors that are better off in this table — say manufacturing or construction — have necessarily grown fast enough over the three years since Covid.

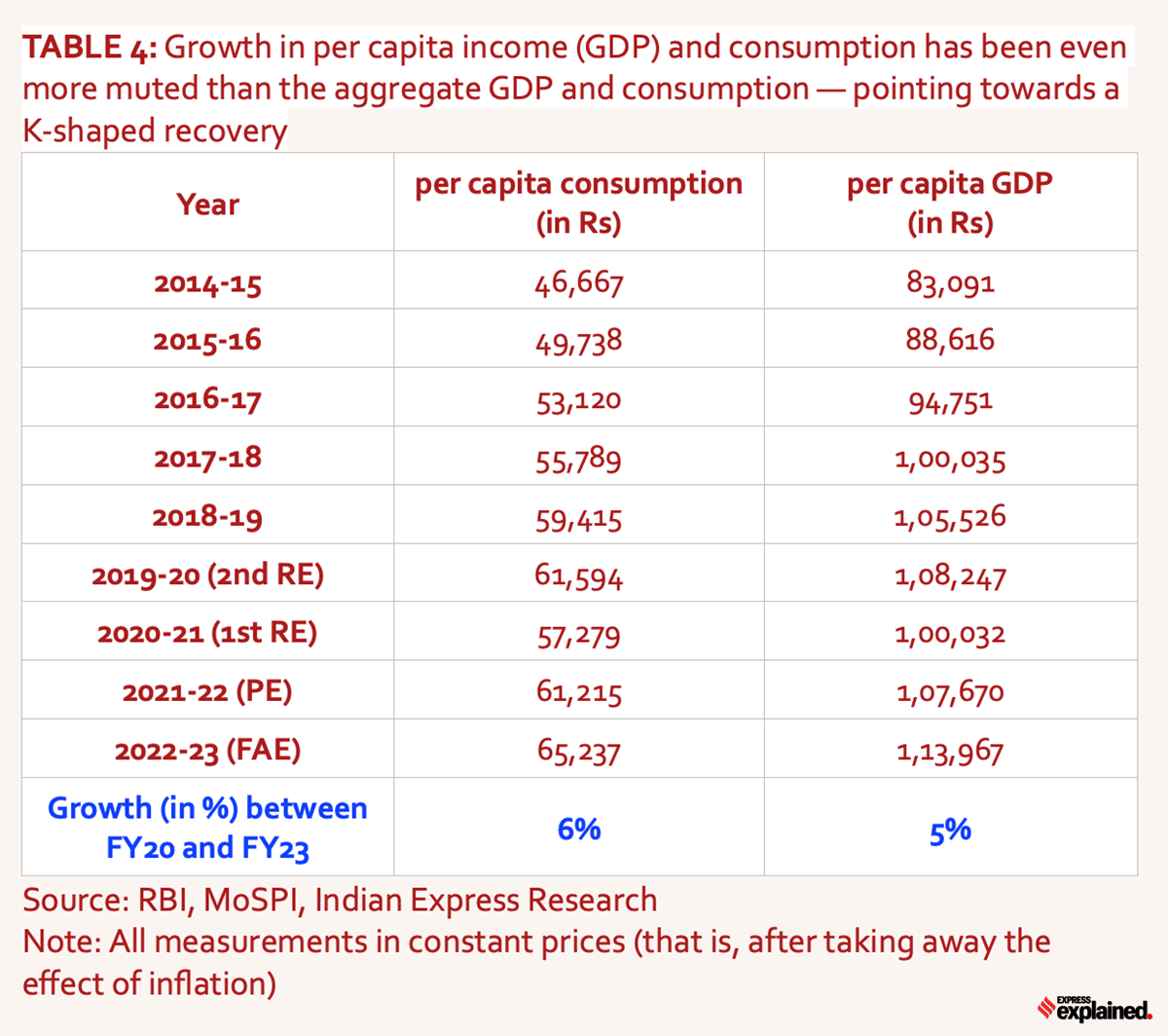

Per capita income and consumption

The reason why one must always look at per capita income and consumption is that aggregate GDP or consumption figures can often fail to provide the kind of stress that an average India may be facing.

TABLE 4 provides the per capita income and consumption levels. As the data shows, growth in per capita income (GDP) and consumption has been even more muted than the aggregate GDP and consumption.

Table 4: Per capita GDP and per capita consumption from FY 15 to FY 23

Table 4: Per capita GDP and per capita consumption from FY 15 to FY 23

This essentially points towards a K-shaped recovery where the better-off sections of India are recovering faster while the worse-off sections of the economy continue to struggle.

To be sure, even per capita numbers — which are arithmetic means — only point towards the stress; looking at median levels of incomes and consumption might do a better job of understanding the coarse reality of India’s economy.

The median, as against the arithmetic mean, is the level below which half the population falls. So while the per capita income of 100 people may be Rs 1,000, it is quite possible that the median income is Rs 100. In other words, 50 people earn less than Rs 100 in this example.

This brings us back to issues of inequality, unemployment and poverty but that is a topic for another day.

Do you think India’s growth is adequately fast or does India require much faster growth rates? Share your views and queries with me at [email protected]

Until next week,

Udit