Rising interest rates in the Indian economy made fixed deposits (FD) attractive in the past year but as experts see the rate hike cycle coming to an end, the big question is: is now a good time to invest in FDs? Or shall we wait a while more?

Rising rate cycle

Since May 2022, the Reserve Bank of India (RBI) has increased the repo rate, the rate at which it lends money to banks, by 225 basis points (bps). That was a clear signal to all market participants that rates were headed higher.

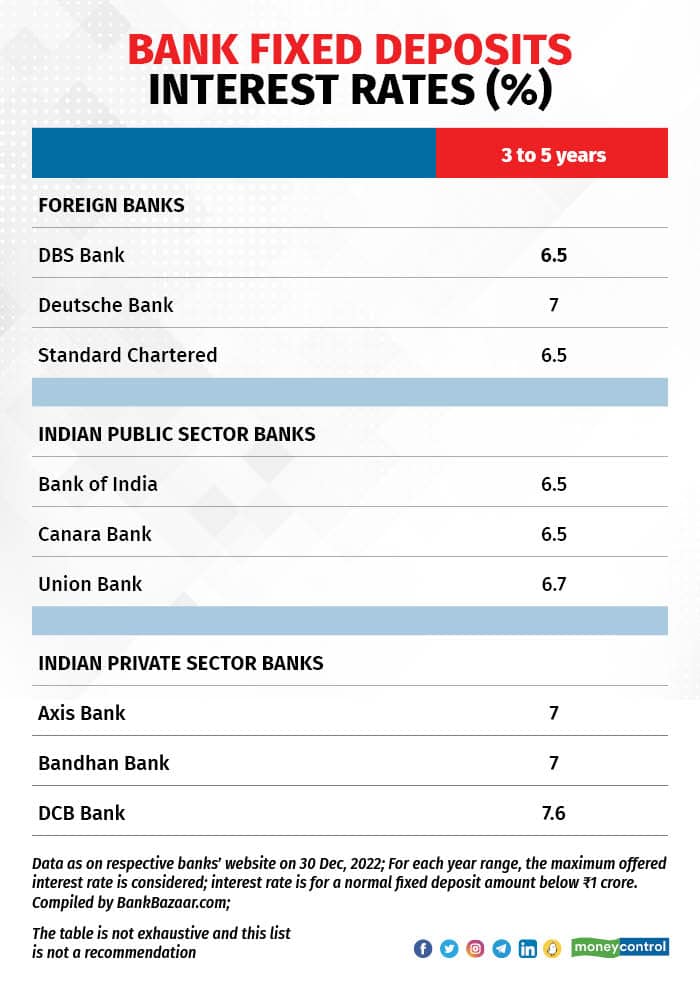

FD rates went up too, even though slower than depositors expected. For example, over the same period of time, leading banks raised FD rates by 130-195 basis points, per BankBazaar data. These are FDs maturing in one to three years, the popular ones among FD investors.

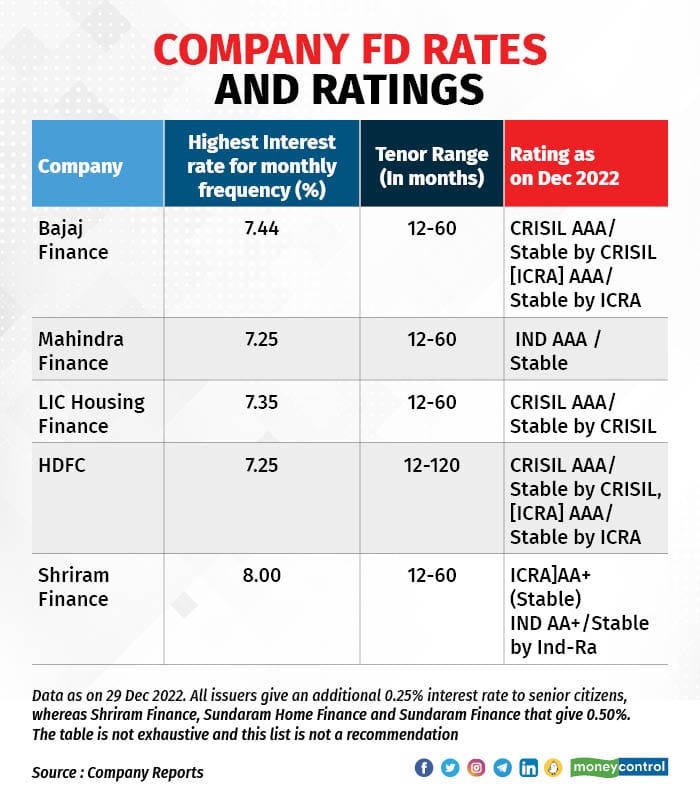

Generally, non-bank finance companies (NBFC) and housing finance companies (HFC) tend to offer a tad more than what’s offered by banks to attract retail money. For example, HDFC, an HFC, offers an interest of 7.3 percent on a 15-month FD, compared to HDFC Bank, which offers 7 percent for a similar tenure.

FD Rush

For investors, FDs make sense if your FD beats inflation. The return on an investment—an FD in this case— in excess of inflation is its real rate of return. If it’s positive, you’ll have something left after adjusting for inflation, and your money will be gaining value. A negative real rate of return means inflation is chipping away at the real value of your cash.

High inflation in India has made policymakers increase interest rates. No wonder, some investors jumped to grab the high interest rates offered. For example, HDFC Sapphire Deposits, which launched in October 2022 for a period of 45 months and offered 7.5 percent interest (now 7.6 percent), was lapped up.

While rising interest rates made investors consider FDs, the tepid performance of equity mutual funds (MF) in the recent past has also been a reason for investors to embrace FDs. According to Value Research, flexicap funds on average lost 2.09 percent in the year ended 5 January 2022.

“A small number of investors are shifting money from mutual funds (MF) to corporate FDs. Many conservative investors also shifted from low-interest bank FDs to relatively higher-interest, good quality corporate FDs,” says Anup Bhaiya, Founder of Mumbai-based Money Honey Financial Services. “If HDFC offers better rates than HDFC Bank, then most find it attractive to allocate some money to HDFC FDs,” he adds.

Parul Maheshwari, a Mumbai-based certified financial planner (CFP) has seen many investors switch from bank FDs to corporate FDs in the last six months. “Most well-advised MF investors come with a long-term view and they seldom shift to FDs just because of one year of poor returns,” she added.

ALSO READ: ‘Either or survivor’ clause in bank FDs a myth; surviving joint-holder has a Herculean task on hand

Will rates rise further?

Though investors have been benefitting from the high interest rates, there is not much upside left, say experts. “One more hike in repo rate by the RBI is expected in the near future, and there is a possibility of some upside in interest rates offered on bank FDs,” said Joydeep Sen, Corporate Trainer, Debt.

Rates offered on small saving schemes were hiked last week. However, short-term rates were hiked more than long-term rates. The rates on one-year FDs went up by 110 basis points to 6.6 percent, while five-year National Saving Certificate (NSC) rates were hiked by 20 basis points to 8 percent. Public Provident Fund (PPF) and Sukanya Samriddhi Yojana rates were left unchanged. The tinkering indicates that long-term rates are fairly priced in. And that partly answers the question posed by many investors if it is a good time to lock in their money at current interest rates.

What should you do?

Though it is a good time to invest in long-term FDs, do not go overboard. “Keep your short-term emergency funds in your bank FD and ladder some money in corporate FDs. Laddering helps overcome reinvestment risk,” says Bhaiya. More importantly, do not take credit risk in search of high returns. In search of a couple of percentage points more, investors may run the risk of losing their entire capital, he adds.

Laddering involves investing in FDs of varying maturities, ensuring cash flows at various points of time, say at one, three, and five years. Reinvestment risk refers to the possibility that an investor may be unable to reinvest the interest and principal received at a rate comparable to their current rate of return.

Many investors have come upon juicy NCDs (non-convertible debentures) offering up to 9 percent interest. However, investors have to be careful while selecting them. Maheshwari points out that, “These NCDs carry AA or lower rating, indicating higher credit risk compared to AAA rated quality FDs. Also, many investors find it difficult to overcome the operational challenges of applying for NCDs due to the compulsory issuance of NCDs in demat format.”

Conservative investors, especially senior citizens, may not have demat accounts, they may find it difficult to make payments using digital means. In some cases the limited window of public issue makes it difficult to arrange funds and complete the process.

ALSO READ: IIFL Finance NCD issue offering up to 9% yield opens; should you invest?

Since NCDs are listed on stock exchanges, investors can sell them in the secondary market if the need arises. However, there is no guarantee that these find buyers and at a fair price. Comparatively, FDs are fairly liquid in most cases, with clearly-stated premature withdrawal penal charges and a lock-in period (in some cases).

ALSO READ: InCred Financial’s NCD issue offers higher rates for shorter durations. Should you invest?

If you are an investor in a low-income tax slab, then FDs make sense for you. Since the interest is taxed per the slab of the investor, most high income earners prefer to stay with debt funds.

“Though debt funds have given low single-digit returns in the past one year, the yield-to-maturity of debt funds has gone up in line with rising yields. Hence, from a post-tax returns point of view, good quality bonds, along with target MFs can be considered over traditional FDs by investors in high income tax slabs,” said Sen.

While choosing FDs, double check the terms pertaining to premature withdrawal and do not chase high yields.