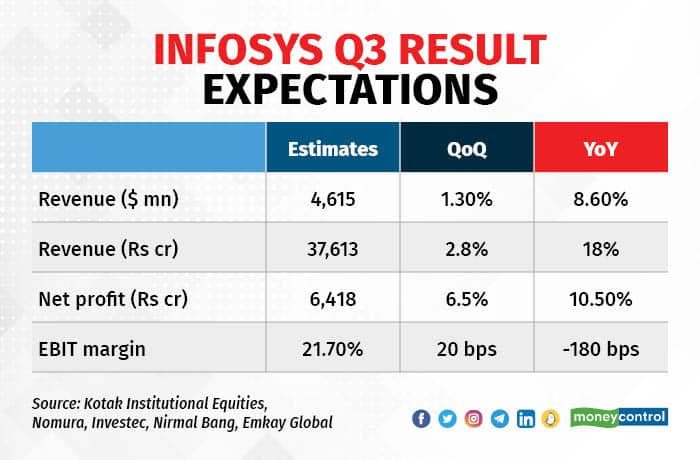

After Tata Consultancy Services (TCS) failed to meet Street expectations, all eyes are now on blue-eyed boy Infosys’ October-December results on January 12. The once IT bellwether is expected to report a 2.8 percent quarter-on-quarter (QoQ) growth in revenue while net profit is expected to increase 6.5 percent QoQ.

According to a poll of brokerages, the consolidated revenue of the second-largest information technology (IT) company might come in at Rs 37,613 crore, registering 18 percent year-on-year (YoY) growth, while consolidated profit after tax (PAT) is expected to increase 10.5 percent YoY to Rs 6,418 crore.

In constant currency (CC) terms, analysts forecast a revenue growth of 1.1 percent QoQ. “High furloughs and lack of large deal kicker, unlike previous two years, will result in muted growth,” said Kotak Institutional Equities’ analysts.

Margins stable

Brokerages are largely of the view that EBIT (Earnings Before Interest and Tax) margins will remain stable, with a modest 20 basis point expansion QoQ to 21.70 percent. One basis point is one-hundredth of a percentage point.

Margin expansion that would have come on the back of rupee depreciation will be partially offset by furloughs, noted Investec Securities. Attrition is set to moderate further as supply-side pressures ease, it added.

Amid recessionary pressures, total contract value (TCV) and new deal wins of the company will be keenly watched. Infosys’ peer TCS in its Q3 results flagged off tightening client spends in Europe. Its order book for the quarter stood at $7.8 billion, while Street’s expectation was $9 billion.

Large deals and guidance

For Infosys, analysts at Nirmal Bang Institutional Equities are forecasting TCV deals of $2 billion, reflecting a QoQ decline. The company’s large TCV deal wins stood at $2.7 billion in Q2FY23, the highest in seven quarters.

Despite the muted numbers, experts believe the management will retain its revenue and margin guidance. Earlier, the IT giant had raised the lower end of FY23 revenue guidance to 15-16 percent in CC terms from 14-16 percent. However, margin guidance was narrowed down to 21-22 percent from 21-23 percent.

Factors to consider

According to Emkay Global, here are the other factors investors should keenly monitor.

-Any delay/deferral/cancellation of projects due to macro uncertainties and high inflation

-Update on client conversations – impact from high energy prices, inflation and potential economic slowdown/recession

-Management commentary on the CY23 IT budget

-Demand environment in manufacturing, retail, communications, and banking and financial services

-Deal closure momentum

-Hiring trends and attrition rates

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.