Tata Consultancy Services

Tata Consultancy Services (TCS) shares declined more than 2 percent intraday on January 10, a day after the company released its December quarter (Q3FY23) earnings.

Tata Consultancy Services on January 9 reported a 10.98 percent increase in its consolidated net profit at Rs 10,883 crore for the quarter ended December 2022 (Q3FY23). The company had posted a profit of Rs 9,806 crore in the year-ago period.

The consolidated revenue from operations came in at Rs 58,229 crore, up 19.11 percent against Rs 48,885 crore in the corresponding quarter of the previous fiscal.

Tata Consultancy Services was quoting at Rs 3,239.30, down Rs 80.40, or 2.42 percent on the BSE.

In constant currency terms, the revenue rose 13.5 percent year-on-year (YoY), the company said, adding that growth was led by North America and thre UK, which rose 15.4 percent on-year. Operating margin stood at 24.5 percent -contracting by 0.5 percent YoY. Net margin came in at 18.6 percent.

Catch all the market action on our live blog

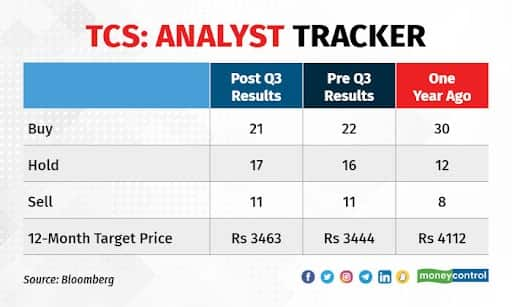

Here is what brokerages have to say about stock and the company after the December quarter earnings:

Bernstein

The brokerage house has kept the ‘outperform’ rating on the stock with a target at Rs 3,840 per share.

The company posted resilient performance as it beat the revenue, while margin was in-line.

The commentary was constructive on North America and the UK, while Europe outlook was weak, while despite macro challenges, the qualified pipeline grew on QoQ.

The broking house remain positive and expect market share gains for scaled full service players, reported CNBC-TV18.

Citi

The research firm has maintained the ‘sell’ rating on the stock with a target at Rs 2,990 per share.

According to the firm, the Q3 was in-line, adjusted for growth in regional markets.

The book to bill was at 1.1x in Q3 versus 1.35x in FY22, the growth in ex-regional markets was at 1.2 percent QoQ. The headcount declined QoQ, and expect a muted Q4 as well.

The BFSI growth slowed to over 1 percent QoQ and over 11 percent YoY.

Citi feels that the company could be defensive in a tough environment given cost controls, while difficult to see upside at 25x FY24e; 7 percent FY22-25 EPS CAGR, reported CNBC-TV18.

JPMorgan

The broking firm has remained ‘underweight’ on the stock with a target at Rs 3,000 per share.

The book-to-bill is declining, while net hiring is negative. The stock trades at 26x 1-yerr forward P/E, 30 percent premium to pre-COVID.

Its 5-10-yerr average looks unjustified given worsening macro & continued slowdown, reported CNBC-TV18.

Nomura

The brokerage house has kept ‘reduce’ rating on the stock with a target at Rs 2,850 per share after modest revenue beat, but margin was a miss.

Broking firm feels that the near-term visibility remains low. The margin improvement continued, and easing supply side to aid margins.

Nomura believes that the growth to lag Infosys; and no meaningful changes to earnings, reported CNBC-TV18.

Morgan Stanley

Research house has kept equal-weight on the stock with a target at Rs 3,350 per share.

The revenue was beat but weak book-to-bill ratio. The constructive commentary on North America, balanced by weak outlook for Europe.

There was a miss on margin, but good outlook for Q4.

The research house maintained the FY24/25 EPS estimates and expect near-term sentiment to be positive, reported CNBC-TV18.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.